Different Strokes

Two of the world’s largest companies are spending money at a pace that would make a central banker blush. Amazon and Meta are each pouring tens of billions into AI infrastructure annually — numbers so large they’ve stopped feeling real. Wall Street is broadly bullish on both. The narrative is simple: AI is the future, and these two are buying it.

I’m bullish on one and bearish on the other. Here’s why.

Same Bet, Different Destinations

Let’s start with what they have in common. Both Amazon and Meta are spending aggressively on AI data centres, chips, and infrastructure. Both are household names with enormous balance sheets. Both have CEOs who speak about AI with near-religious conviction.

Strip away the surface similarities, and two completely different stories emerge.

Amazon knows exactly where it’s going. Meta is still looking for the exit on the highway.

The Landlord Nobody Saw Coming

The consensus Amazon bull case is well-worn by now. AWS. Cloud dominance. Picks and shovels. Everyone owns it for roughly the same reasons.

But the more interesting story isn’t the one being told on every investment podcast. It starts with a quiet admission.

Amazon tried to play in the AI model game. They launched Amazon Nova — their own family of foundation models — with genuine ambition. It didn’t work. Nova became the second most popular model family on their own platform. The first? Anthropic’s Claude. Amazon built the restaurant, hired the chef, and discovered their customers kept ordering from the place next door.

Most companies would double down out of ego. Amazon did something smarter. They took their ball and went home.

And in doing so, accidentally — or perhaps deliberately — became the most strategically positioned company in the entire AI race.

The Neutral Racetrack

Here’s what nobody was talking about when Amazon quietly shelved their frontier model ambitions: every serious AI lab suddenly had a problem.

OpenAI couldn’t train on Microsoft’s infrastructure without feeding a company that was simultaneously competing with them through Copilot. Google was building Gemini in-house — no frontier lab was going to hand their training workloads to a direct model competitor. The AI industry was verticalising fast, and the independent labs were running out of neutral ground.

Amazon, precisely because Nova had lost convincingly, became the safe harbour. No dog in the model fight. No conflict of interest. Just infrastructure, at scale, with no agenda.

Anthropic came first. Then came OpenAI — in a deal that would have been unthinkable two years ago. Amazon invested $50 billion in OpenAI. OpenAI committed to consuming two gigawatts of Trainium capacity through AWS. AWS became the exclusive third-party cloud distribution provider for OpenAI’s enterprise platform.

Let that sink in. The two most important frontier AI labs in the world — fierce competitors — are both training their models on Amazon’s infrastructure.

The landlord doesn’t care who wins. The landlord collects rent either way.

The Rent Keeps Coming

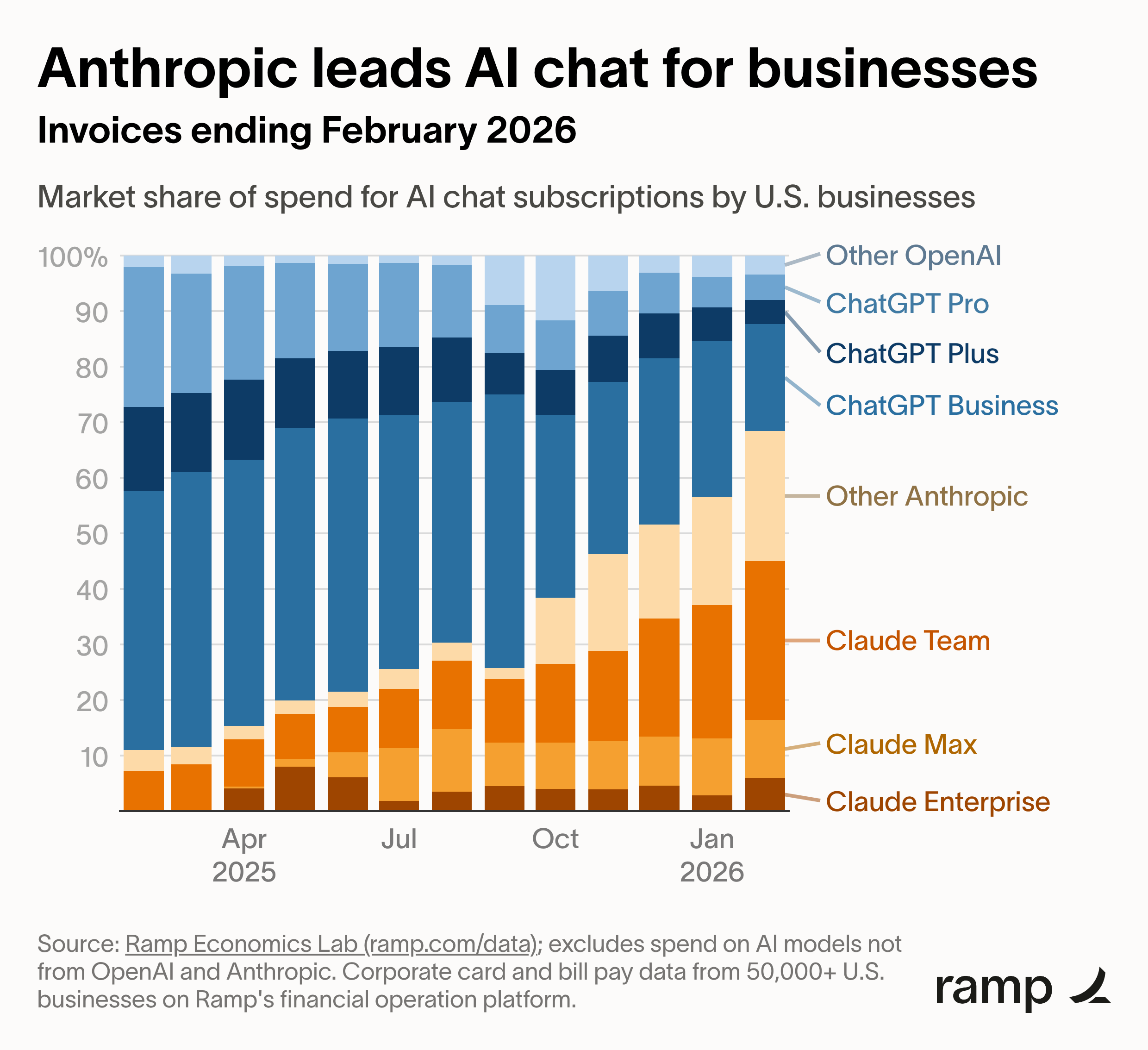

Look at what’s happened in the enterprise AI market over the past twelve months.

Anthropic has gone from a sliver of business AI spend to commanding the majority of it by early 2026. Claude Team is the dominant driver. ChatGPT — which owned 80% of this market not long ago — has been compressed into the top third.

This chart is proof of concept for the Amazon landlord thesis. Every dollar a business shifts from ChatGPT to Claude is more inference revenue, more Bedrock usage, more Trainium demand flowing through AWS. Anthropic’s run-rate revenue recently surpassed $30 billion. The compute bill for generating that revenue? It goes to Amazon.

The labs can race each other to the bottom on pricing. They can offer free tiers, enterprise discounts, aggressive contracts. That’s their problem. Amazon’s Trainium chips get used regardless of who’s winning. The compute bill lands on the same desk either way.

The Longer Game

I can’t prove this, but it’s something I’ve thought about.

AI models are getting better at recommendations. We’re not far from a world where, instead of typing “best toaster” into Google, you ask Claude or ChatGPT to recommend one — and it does, with specifics, with links, with purchase options.

Who controls what those models recommend? And who benefits if the recommendation points to a particular marketplace?

Amazon has invested billions into both Anthropic and OpenAI. They are the primary infrastructure partner for both. I’m not suggesting there’s a backroom deal. But when you’re the landlord, the financier, and the infrastructure provider for the companies building the recommendation engines of the future — and you also happen to run the world’s largest e-commerce marketplace — that’s not a conflict of interest. That’s a hedge.

Maybe Amazon is playing a longer game than anyone realises.

The Warehouse Nobody’s Talking About

But even if none of that speculation proves true, the most compelling part of the Amazon story has nothing to do with AI models at all.

Amazon spent twenty years building one of the most complex logistical infrastructures in human history. Hundreds of fulfilment centres. Over a million robots already deployed — a fleet approaching parity with their human workforce. A last-mile delivery network that rivals national postal services. Three in four Amazon deliveries are now assisted by robotics in some form.

AI and robotics don’t disrupt this. They turbocharge it.

Amazon has already launched DeepFleet — a generative AI model that coordinates robot movement across its entire fulfilment network. The first version improved robot fleet travel time by 10%. That’s not a headline number. But applied across a million robots and hundreds of facilities, it compounds into something significant very quickly.

Every incremental improvement in warehouse automation, route optimisation, demand forecasting, and customer service AI flows directly to Amazon’s cost structure. They don’t need a frontier model to win here. They just need the tools to get marginally better at a game they already dominate. The efficiency gains compound quietly, quarter after quarter, in ways that don’t make headlines but absolutely show up in margins.

This is the most concrete, most defensible, least speculative part of the entire Amazon AI story. No lab needs to win. No chip needs to dominate. The robots just need to get a little smarter.

The Other Side of the Bet

Meta is spending $135 billion on AI capital expenditure in 2026 alone.

Let that number breathe for a moment.

From a company whose revenue is almost entirely dependent on digital advertising. From a company with no enterprise AI clients. No cloud business. No third-party training revenue. No one is paying Meta to run their models.

So what exactly is the plan?

Zuckerberg’s answer, when pressed, is that Meta needs to own its own AI because it can’t afford to be “constrained to what others in the ecosystem are building.” That’s not a revenue model. That’s a philosophy. And it’s a philosophy that sounds suspiciously familiar.

Fool Me Once

Cast your mind back to 2021. Apple introduced App Tracking Transparency — a simple toggle that let iPhone users opt out of being tracked across apps. Meta’s stock fell off a cliff. The company warned of $10 billion in annual revenue losses. Zuckerberg, for the first time, looked genuinely rattled.

The reason was structural. Facebook had built its entire advertising empire on data it didn’t own, flowing through pipes it didn’t control. The moment Apple flipped a switch, the tap ran dry. Meta was a tenant who had confused the landlord’s house for its own.

What followed was the metaverse — billions spent trying to build a platform Zuckerberg owned outright, where Apple and Google couldn’t touch him. His own hardware. His own operating system. His own digital world. Reality Labs has now accumulated nearly $90 billion in operating losses. Nobody uses the metaverse. Zuckerberg didn’t say the word once in his most recent earnings call.

Before that, there was the Facebook phone. Same instinct. Different vehicle. Total failure.

Now it’s AI infrastructure, and a quote that should give every Meta shareholder pause. Zuckerberg does not want to be beholden to anyone else’s AI model. He wants to control the stack.

The pattern is clear. Every time Zuckerberg feels dependent on an infrastructure he doesn’t own, he spends extraordinary amounts of money trying to build his own. Sometimes the market cheers him on. It rarely works.

The Llama Is Dead

Meta’s open-source model Llama deserves credit for one thing: it was first. When Llama arrived, it was a genuine moment — a usable, open-source model that democratised access to large language model technology. The AI community celebrated it. In October 2024, Zuckerberg proclaimed “Open Source AI is the Path Forward” and meant it.

That was then.

The flagship Llama 4 “Behemoth” model was shelved after underperforming on critical benchmarks, leaving Meta without a competitive answer to rivals. And then came the detail that should haunt every Meta shareholder: DeepSeek — a Chinese lab — used Llama as a foundation to build models that leapfrogged it entirely. Meta spent years building open-source AI infrastructure and handed the competition their own playbook.

The response? Meta quietly abandoned Llama altogether. They launched Muse Spark — a closed, proprietary model built from scratch on entirely different infrastructure and architecture. The open-source manifesto, the billion downloads, the developer ecosystem — gone. Starting over.

Here’s what makes this particularly uncomfortable: the open-source strategy was supposed to be Meta’s moat. The thing that made developers dependent on their ecosystem. DeepSeek collapsed that thesis. So Meta pivoted to closed-source — directly competing with OpenAI and Anthropic, companies with a three-year head start, hundreds of enterprise clients, and models that Muse Spark currently benchmarks below.

And unlike Amazon, there is no elegant retreat available. No infrastructure business to fall back on. No training revenue to collect. No landlord position waiting in the wings. Just a very expensive restart, funded by an ad business that has nothing to do with any of this.

Bottom Line

Two giants. One bet. Completely different odds.

Amazon stumbled into the best strategic position in AI by failing gracefully at the model game. Their capex has a clear return path — training revenue, inference revenue, and a warehouse automation story that compounds quietly in the background. The landlord collects rent regardless of who wins the model war. And if my speculation about AI-driven product recommendations is even half right, the upside gets more interesting still.

Meta is running the same play it has run twice before — spending aggressively to escape dependency on infrastructure it doesn’t control. The metaverse was the last version of this film. We know how it ended.

I could be wrong about Meta. Zuckerberg has surprised markets before, and the ad business is strong enough to absorb significant losses while the AI bet plays out. But the rope is very long, and history suggests he’ll find a way to hang himself with it.

I know which one I’d rather own.