Uneducated Investor Q1 2026 Portfolio Update

I’ve had some new subscribers recently, so I thought it would be a good time to write a portfolio update — what I’m in, what’s on my radar, and the thinking behind it all.

For new subscribers, the first thing you need to know is — I’m not an educated man. Never went to Wharton or Harvard. No financial degree. No work experience in finance – never even been to Wall Street. If you’re looking for a credentialled expert, you’re in the wrong place. If you’re looking for an honest, independent perspective from someone who puts their own money where their mouth is, read on.

Performance

I believe in transparency. So before anything else, here are the numbers — pulled directly from my Interactive Brokers account.

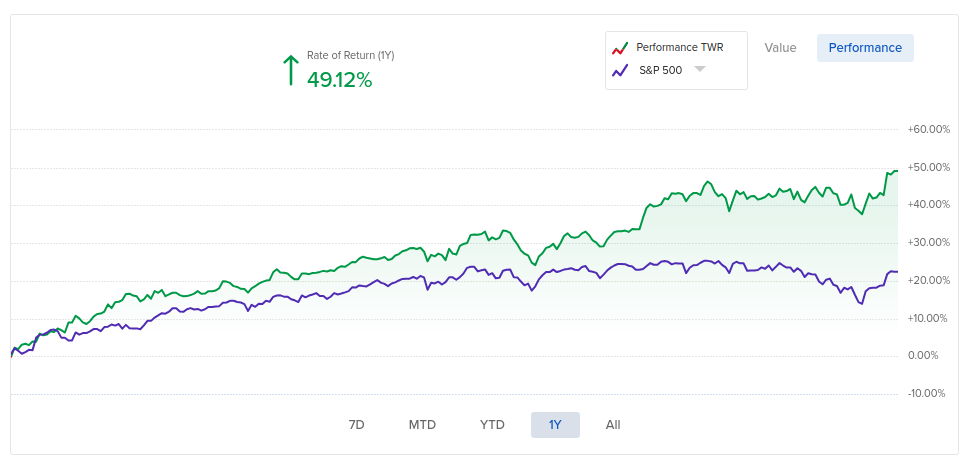

YTD 2026

| Period | Portfolio | S&P 500 |

|---|---|---|

| YTD 2026 | +11.57% | -0.4% |

1 Year

| Period | Portfolio | S&P 500 |

|---|---|---|

| 1 Year | +49.12% | +22.4% |

I share these because accountability is the foundation of this blog’s credibility. I got things right. I got things wrong. The goal isn’t to win every trade. It’s to never blow up.

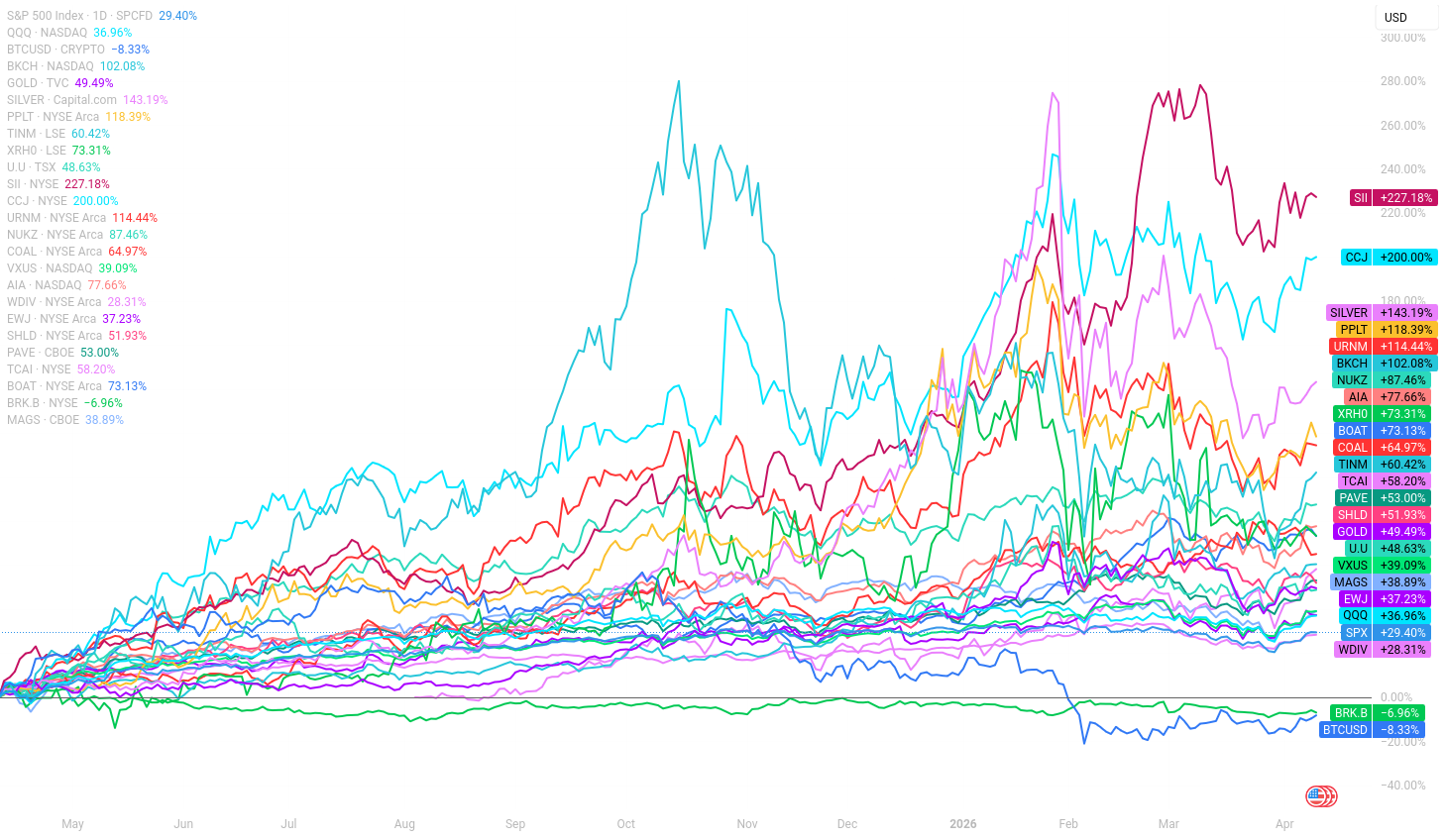

Below is a TradingView chart showing how many of the tickers in this publication have performed against the S&P 500 over the past year.

The Philosophy Behind the Portfolio

Before we get to the holdings, you need to understand the framework. The positions only make sense once you understand the thinking behind them.

Fewer Losers, Not More Winners

The most important investing insight I’ve come across didn’t come from a hot take on X or a YouTube trader. It came from Howard Marks of Oaktree Capital.

Marks once described a pension fund manager named Dave Van Bencoten who ran the General Mills pension fund for 14 years. His equity portfolio was never above the 27th percentile in any given year — but never below the 47th percentile either. Always solidly second quartile. Where did that put him over the full 14-year period? The 4th percentile.

Read that again. Never top-quartile in any single year. Top 4% over the entire period.

The math is counterintuitive, but the logic isn’t. Consistency compounds. Catastrophic losses don’t recover. A fund that drops 50% needs a 100% gain just to get back to even. Most investors never think about this until it’s too late.

Marks put it best with a simple analogy: investing at Oaktree is like eating at his favourite Italian restaurant — always good, sometimes great, never terrible. It’s an unsexy standard. Nobody makes a motivational video about being consistently above average. But sustained for 40 years, it compounds into something extraordinary.

Buy When You Don’t Want To

When the time comes to buy, you won’t want to.

The best opportunities arise at the point of maximum pessimism. When prices are lowest. When headlines are worst. When everyone around you is selling. That’s precisely the moment most investors freeze. It’s the moment I try to act.

It doesn’t feel heroic. It feels uncomfortable. But a battlefield hero isn’t someone unafraid — it’s someone who does it anyway.

The Bus Stop Rule

Investing is like standing at a bus stop. Never chase the bus. Another one is always coming.

Chasing entries is how good returns get destroyed. Discipline about price is non-negotiable. If the move is missed, wait for the next one.

How I Size and Enter Positions

Every position in my portfolio has a target allocation of roughly 3% — what I’d call a regularly-weighted position. If I’m very bullish on something, I’ll go up to 6%. If I’m cautious, I’ll hold as little as 1.5%.

I also tranche in. Instead of putting all my capital to work at once, I buy in stages — typically at the 50, 200, and 800-day EMAs on the daily chart. This means if the price falls further, I can buy more at a lower cost. If it runs, I at least have some skin in the game. I only enter positions that were already in a strong uptrend before a non-fundamental selloff knocked them back. My 5-year thesis on the position needs to remain intact.

Current Holdings

Before we go further, let me be clear about what this section is and isn’t.

This is not a buy list. I am not recommending any of these positions. What I’m sharing is a transparent account of what I personally own, each of which I’ve written about in depth elsewhere on this publication. The blurbs below are brief by design — a starting point, not a conclusion. If something catches your eye, that’s your cue to do your own research and form your own view.

Not everything here has worked. I’m down badly on cocoa. I’m underwater on Bitcoin. And that’s fine — because this is where the philosophy from earlier stops being theory and becomes practice. A 3% position that halves costs you 1.5% of your portfolio. That’s recoverable. A concentrated bet that goes wrong can set you back years. Position sizing isn’t just risk management. It’s survival. Howard Marks wasn’t talking about avoiding all losers. He was talking about making sure your losers can’t kill you.

Here’s what I own right now, organized by theme.

⚡ Coal

COAL (Range Global Coal Index ETF — AMEX)

Everyone hates coal. That’s exactly why I own it. ESG mandates have forced institutional money out of the sector entirely, creating a valuation gap that the fundamentals don’t justify. China and India are building coal plants at record pace. Watch what countries do, not what they say. COAL is a passive ETF tracking global coal producers across metallurgical and thermal coal.

₿ Bitcoin

IBIT (iShares Bitcoin Trust ETF — NASDAQ)

I own Bitcoin, but I own it through BlackRock’s IBIT — the world’s largest and most liquid spot Bitcoin ETF. No wallets, no seed phrases, no exchange counterparty risk. Just clean, regulated exposure through a brokerage account. The thesis is straightforward: Bitcoin is a scarce, decentralised asset with growing institutional adoption. IBIT makes that thesis accessible without the operational headaches of self-custody. I’m currently underwater on this position. I’m not panicking. A 3% allocation bought in tranches means I can weather volatility without it derailing the portfolio.

☢️ Uranium & Nuclear

U.U (Sprott Physical Uranium Trust — TSX)

Not miners. The metal itself. Sprott’s Physical Uranium Trust holds physical uranium in storage, giving direct exposure to the uranium spot price. With global demand expected to roughly double by 2040 and supply chronically undershooting reactor requirements, the structural case is compelling. This is the cleaner, more direct expression of the uranium thesis.

URNM (Sprott Uranium Miners ETF — NYSE Arca)

The miners amplify the thesis. URNM provides concentrated exposure to pure-play uranium mining companies globally. When uranium prices move, miners move further — in both directions. I hold this alongside U.U to capture operating leverage on the commodity move.

NUKZ (Range Nuclear Renaissance Index ETF — NYSE Arca)

A broader bet. NUKZ covers the full nuclear ecosystem — utilities, fuel, advanced reactor companies, and service/construction firms — not just uranium miners. As the energy transition collides with the AI power demand shock, nuclear is being reassessed as a serious baseload solution. NUKZ captures that repricing across the entire value chain.

🛢️ Soft Commodities

COCO (WisdomTree Cocoa — LSE)

After a historic cocoa supply shock drove prices to record levels in 2024, the commodity corrected sharply in 2025. I entered COCO as a contrarian play on the recovery. West African supply disruptions haven’t fully resolved, and cocoa remains one of the more interesting soft commodity setups for patient investors. I’m currently down significantly on this position. The thesis remains intact. The 3% allocation means it’s painful but not damaging.

🥇 Metals

GOLD (Gold spot exposure — CapitalCom)

Gold is a core macro hedge. In a world of mounting government debt, geopolitical fragmentation, and central banks buying at record pace, the case for gold as a portfolio anchor remains intact. I’ve been careful about timing given competing forces, but the structural tailwinds aren’t going away — and neither is my position.

PPLT (Aberdeen Physical Platinum Shares ETF — NYSE Arca)

Platinum is the unloved sibling of the precious metals family. Historically priced at a premium to gold, it now trades at a steep discount. Platinum has industrial applications in hydrogen fuel cells and catalytic converters, and supply is heavily concentrated in South Africa. A structural case for mean reversion, with optionality on the green energy transition.

XRH0 (WisdomTree Physical Rhodium — LSE)

Rhodium is the most obscure metal in my portfolio and one of the most interesting. Used almost exclusively in automotive catalytic converters, it’s produced almost entirely as a by-product of platinum group metal mining in South Africa. Supply cannot respond quickly to price. It’s illiquid, volatile, and misunderstood — exactly the profile I look for in a contrarian play.

TINM (WisdomTree Tin — LSE)

Tin is the forgotten industrial metal. It’s critical for solder — which means it’s in every circuit board, every semiconductor, every piece of electronics manufactured on earth. Demand is structural and growing. Supply is constrained. It doesn’t get column inches, which suits me fine.

🌏 Asia

AIA (iShares Asia 50 ETF — NASDAQ)

Broad exposure to 50 of the largest equities across the Asian Tiger economies: Hong Kong, South Korea, Singapore, and Taiwan. My macro view is that Asia ex-China is structurally undervalued relative to the US, particularly as capital diversifies away from a US-centric world. AIA is my anchor for that thesis.

HKEX:142 (First Pacific Company — Hong Kong)

First Pacific is a Hong Kong-listed investment holding company with operations across Southeast Asia spanning telecommunications, infrastructure, food, and natural resources. It’s a classic conglomerate play on Asian consumer and infrastructure growth, trading at a discount to the sum of its parts.

EWJ (iShares MSCI Japan ETF — NYSE Arca)

Japan is having a moment — and I think it has more runway. Corporate governance reforms are unlocking shareholder value that was trapped for decades. The weak yen has driven export competitiveness. Buffett’s well-publicised investment in Japanese trading houses validated what contrarians already knew. EWJ gives me clean, broad access to this story.

HKEX:3067 (iShares Hang Seng Tech ETF — Hong Kong)

China tech has been left for dead by Western investors. I disagree with the consensus. The Hang Seng Tech Index holds the largest and most liquid Hong Kong-listed technology companies — Tencent, Alibaba, Meituan, and others. The regulatory crackdown cycle appears to be over, valuations are a fraction of US equivalents, and domestic AI development is accelerating. 3067 is my vehicle for that re-rating.

TSE:2033 (KOSPI 200 Leveraged ETF — Tokyo)

The Korean stock market took a severe beating as a consequence of the US-Iran war and the oil price spike that followed. This is a leveraged play on the KOSPI 200 — South Korea’s large cap index — bought into that weakness. Korea has deep exposure to semiconductors, shipbuilding, and manufacturing. None of that changed because of a geopolitical event on the other side of the world. The thesis here is simple: when a quality market sells off for non-fundamental reasons, you run toward it. Could it go lower? Absolutely. But when the potential downside is 10-15% and the upside is 60-90%, I’ll take that bet.

🌍 Global ETFs

VXUS (Vanguard Total International Stock ETF — NASDAQ)

My ex-US diversification anchor. VXUS holds over 8,500 equities across developed and emerging markets outside the United States. As I’ve written before, I think the decade of US equity dominance is showing signs of aging. VXUS is a low-cost, disciplined way to stay diversified globally.

WDIV (SPDR S&P Global Dividend ETF — NYSE Arca)

Income and geographic diversification in one vehicle. WDIV holds high-dividend-paying equities from around the world. In an era of elevated inflation and uncertain capital gains, dividend income provides a real return floor. It also naturally skews toward sectors and geographies that the growth-obsessed market ignores.

GREK (Global X MSCI Greece ETF — NYSE Arca)

Greece is one of the more surprising performers of recent years, emerging from sovereign debt crisis into a functioning economy with improving fundamentals. I hold GREK as a frontier contrarian position — a country that was left for dead and is quietly rebuilding.

EPOL (iShares MSCI Poland ETF — NYSE Arca)

Poland is a direct beneficiary of European defence spending and NATO expansion. As the geopolitical map of Europe redraws itself, Poland — strategically located, pro-Western, and rapidly modernising — is worth owning. EPOL gives me that exposure cleanly.

EWZ (iShares MSCI Brazil ETF — NYSE Arca)

Brazil has struggled under political and fiscal uncertainty, which has kept valuations suppressed. I see a deep-value case here: a resource-rich economy with world-class agriculture, energy, and mining sectors, trading cheap. The thesis requires patience, but the potential reversion is significant.

UAE (iShares MSCI UAE ETF — NASDAQ)

Same war, same logic as Korea. The UAE market has been hammered by the fallout from the US-Iran conflict despite being a fundamentally different beast from the combatants. The UAE is one of the most sophisticated, well-capitalised economies in the Middle East — a global hub for trade, capital, and talent with structural growth that has nothing to do with who’s firing missiles at whom. When large cap stocks of a quality market are trading at prices not seen in years, you don’t run out of the burning barn. You run in. That’s precisely what Marks meant: when it comes time to buy, you won’t want to. Yes, prices could go lower. But with 10-15% of further downside and 60-90% of upside potential, the asymmetry is compelling.

🤖 AI & Technology

TCAI (Tortoise AI Infrastructure ETF — NYSE)

Rather than betting on which AI model wins, I own the infrastructure that all of them depend on. TCAI is an actively managed ETF focused on energy infrastructure, data centres, and digital components — the picks and shovels of the AI buildout. Power generation, cooling systems, storage. The things that have to exist regardless of which LLM ends up on top.

TSE:3110 (Nitto Boseki Co. — Tokyo)

Nitto Boseki is a Japanese industrial company best known for its glass fibre products — specifically high-performance glass fibre for electronic materials applications. Glass fibre is a critical substrate for printed circuit boards and AI hardware. As AI accelerates semiconductor demand, Nitto Boseki sits quietly in the middle of the supply chain.

TSE:268A (Rigaku Holdings — Tokyo)

Rigaku is one of the world’s leading manufacturers of X-ray analytical instruments. That sounds niche. It isn’t. Advanced semiconductor inspection — including the CoWoS packaging architectures that power AI chips — requires Rigaku’s equipment. As 3D chip stacking becomes the next frontier in semiconductor manufacturing, Rigaku’s inspection tools become indispensable.

MSFT (Microsoft — NASDAQ)

Charlie Munger’s advice was simple: when a great company touches a great price, buy it. When Microsoft’s price touched its weekly 200 EMA, that was my entry signal. Azure, enterprise software, deep OpenAI integration — the moat is self-evident. Sometimes the obvious trade is obvious for a reason.

⚓ Shipping

BOAT (SonicShares Global Shipping ETF — AMEX)

Global shipping is the circulatory system of world trade. It’s chronically underinvested in, deeply cyclical, and largely ignored by mainstream investors. BOAT gives me exposure to the global shipping industry — container, tanker, dry bulk — as a play on the structural reality that the world still needs to move physical goods, and the fleet capacity to do so isn’t growing fast enough.

🏗️ Miscellaneous

PAVE (Global X U.S. Infrastructure Development ETF — CBOE)

Infrastructure spending in the US is a multi-decade story, underpinned by bipartisan political consensus, decades of underinvestment, and the reshoring of supply chains. PAVE holds companies across steel, engineering, construction, and industrial machinery. The physical backbone of the US economy being rebuilt from the ground up.

SHLD (Global X Defense Tech ETF — AMEX)

The world is rearming. NATO spending is rising. European defence budgets are at multi-decade highs. SHLD gives me exposure to defence technology — not just traditional hardware, but cybersecurity, advanced military systems, and the software-defined warfare companies that are defining the next generation of conflict.

Watchlist

Same caveat applies here. These are tickers I’ve either owned in the last year and sold for tactical reasons, or am watching to enter when the price is right. Some I’ve written full articles on. Others I’m still researching. Being on this list means I find the thesis interesting enough to keep watching — nothing more. It is not a buy recommendation. Use it as a launch pad for your own thinking.

⚡ Energy

XES (SPDR S&P Oil & Gas Equipment & Services ETF) — Energy services exposure.

TPYP (Tortoise North American Pipeline Fund) — Energy infrastructure with steady cashflows. A candidate for a framework I’ve been developing around truly uncorrelated assets.

BE (Bloom Energy) — Solid oxide fuel cell technology. A long-term hydrogen and distributed energy play. Think data centers building their own power supply.

GRID (First Trust NASDAQ Clean Edge Smart Grid ETF) — Smart grid infrastructure: modernisation, smart metering, energy storage, power management. The grid most countries run on was built for a different era — electrification, AI data centres, and renewables are all hitting it at once. Long runway.

☢️ Uranium & Nuclear

CCJ (Cameco) — The world’s largest publicly traded uranium producer.

🥇 Metals, Precious Metals & Commodities

SILVER — Precious metals re-entry candidate. Exited ahead of the 2026 crash.

COPX (Global X Copper Miners ETF) — Copper is the metal of electrification.

REMX (VanEck Rare Earth/Strategic Metals ETF) — China controls the overwhelming majority of rare earth mining and processing. Every new geopolitical shock — tariffs, Taiwan tensions, Middle East conflict — adds urgency to Western supply chain independence. The war didn’t weaken this thesis. It strengthened it.

COFF (WisdomTree Coffee — LSE) — Soft commodity with a similar contrarian setup to cocoa.

HKEX:3668 (Yancoal Australia — Hong Kong listed) — A major coal producer paying attractive dividends. The thesis isn’t purely capital appreciation — it’s yield. A hated, overlooked company in an unloved industry, paying you to wait.

SII (Sprott Inc.) — The asset manager behind the physical commodity trusts I use. A royalty on the whole thesis.

₿ Crypto

BKCH (Global X Blockchain ETF) — Crypto infrastructure exposure beyond Bitcoin.

🤖 Technology & AI

SMH (VanEck Semiconductor ETF) — The AI infrastructure supercycle is intact. Hyperscalers have committed hundreds of billions through the end of the decade, chip fabs aren’t in the Middle East, and demand is driven by compute workloads that no geopolitical event can cancel. Sold off on macro fear. The thesis is unchanged.

BOTZ (Global X Robotics & AI ETF) — Was near 52-week highs before the US-Iran war knocked it lower. Nothing about the robotics thesis changed — labour shortages, reshoring, factory automation are decade-long trends. Sold on guilt by association.

🏥 Healthcare

XBI (SPDR S&P Biotech ETF) — AI isn’t replacing the drug — it’s finding it faster. Drug discovery timelines are compressing, clinical pipelines have no sensitivity to oil prices, and the healthcare sector is trading at its deepest discount to the S&P 500 in decades. Beaten up for the wrong reasons.

🏗️ Infrastructure & Defence

EUAD — European defence exposure. NATO members are being pushed to spend more, European governments are responding, and the defence industry is structurally underfunded relative to the demand now coming its way.

FIW (First Trust Water ETF) — I wrote about this in depth in my last article. US water infrastructure — aging pipes, contamination remediation, semiconductor fab demand — has zero connection to oil prices or what’s happening in the Middle East. It was sold off in the broad panic. The most clear-cut “wrong address” selloff on my watchlist.

🌏 Asia

HKEX:1919 (COSCO Shipping Holdings) — A steady dividend play. Bought oversold, sold overbought. The kind of trade the strategy is built for — no heroics, just discipline and yield while you wait.

SGX:1MZ (Nam Cheong Limited) — A micro-cap Malaysian offshore vessel builder. Malaysia’s cabotage policy requires vessels operating in its waters to be locally sourced — meaning every offshore drilling programme in Malaysia is a captive customer. You also get shipyard exposure effectively priced in for free. Anchor shareholders and thin institutional coverage keep it off most radars.

A Final Word

Markets are humbling. Every time you think you’ve figured something out, they find a way to remind you that you haven’t. I’ve had positions that looked brilliant turn against me, and positions I nearly didn’t take become some of my best performers. The goal was never to get rich fast — it’s to stay in the game long enough that compounding does the heavy lifting.

That’s why the philosophy matters more than any individual trade. Position sizing, patience, buying when it’s uncomfortable, and never letting a single position do enough damage to set you back years — these aren’t exciting principles. But they’re the ones that keep you in the game.

As Howard Marks said: if you can be always good, sometimes great, and never terrible — and sustain that for decades — the compounding takes care of the rest.

That’s the plan.